Buy Now, Pay Later has crossed the line from payment novelty to regulated consumer credit, and it has done so at a different pace in every major market. As of 2026, Australia and the Gulf states regulate BNPL as consumer credit, the UK and the European Union are landing comprehensive regimes within months of each other, Southeast Asia spans everything from voluntary codes to new licensing laws, India has folded BNPL into its digital lending framework, Brazil has chosen a deliberately light touch, and the United States has reversed the rule it wrote only a year earlier. The product is the same everywhere. The rulebook is not. For any merchant selling across borders, that single fact is now the defining feature of offering installment payments at checkout.

What is Buy Now, Pay Later, and why does its legal status keep changing?

Buy Now, Pay Later is a short-term financing option that lets a shopper take goods immediately and repay in installments, most commonly in three or four payments over a few weeks, usually interest-free if payments are made on time. A third-party provider pays the merchant the full amount upfront, less a fee, and collects from the customer over the repayment schedule. The merchant is paid in full and does not carry the credit risk.

Its legal status keeps shifting for a structural reason. The dominant "pay-in-four" model carries no finance charge and repays in four or fewer installments, exactly the design that historically fell outside consumer credit law, because those rules were written for interest-bearing products. That gap is now closing market by market, because BNPL has grown large enough that regulators treat it as mainstream credit rather than a checkout convenience.

How big is the global BNPL market in 2026?

The global BNPL market reached roughly US$560 billion in gross merchandise value in 2025, a 13.7% increase year on year, and is forecast to approach US$912 billion by 2030 at a compound annual growth rate of about 10.2%. User numbers tell the same story: roughly 380 million people used BNPL in 2024, a figure projected to climb toward 670 million by 2028.

Despite that scale, BNPL still accounts for only about 5% to 6% of global e-commerce payment value, which is why it remains a secondary method overall even as it dominates specific markets. Asia-Pacific is the largest region by provider revenue at roughly 36%, while North America holds the largest share of provider revenue by company base (based on company headquarters rather than where the shopping occurs). The growth phase has also shifted in character. After a 21.7% compound growth rate between 2021 and 2024, the market is maturing into a slower, profitability-focused phase, which is exactly the environment in which regulators tend to step in.

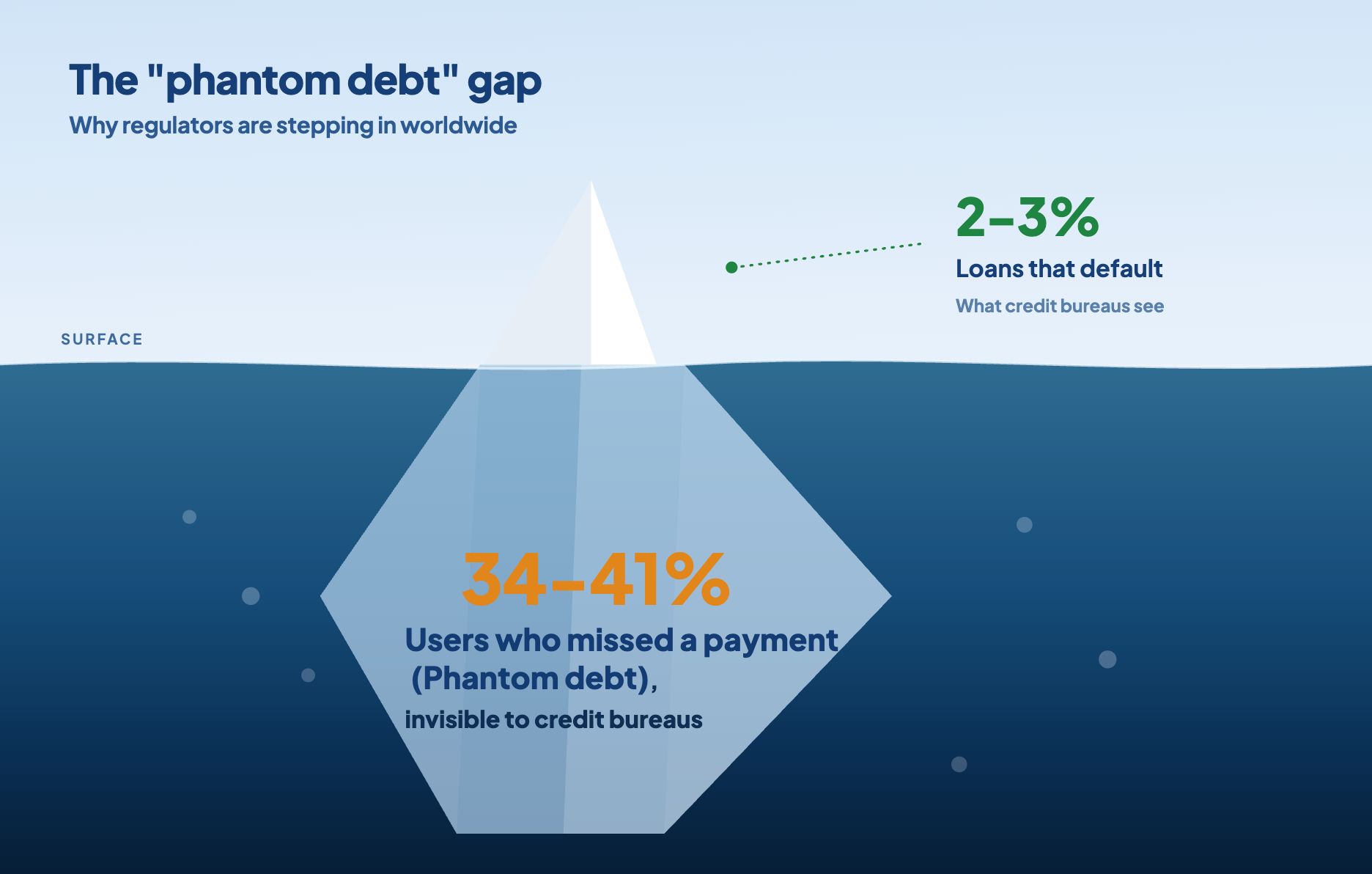

One number explains regulatory urgency better than any growth forecast. Default rates remain relatively contained at around 2% to 3%, but somewhere between 34% and 41% of users report making at least one late payment in the past year. That gap, between low headline defaults and widespread missed payments, is the "phantom debt" concern driving affordability rules across multiple jurisdictions: regulators worry about debt that is real to households but partly invisible to credit bureaus.

How does BNPL help merchants grow revenue?

For merchants, BNPL is not a payments feature; it is a conversion and basket-size lever. It works on three levers at once.

It lifts conversion by removing price friction at the moment of decision. A shopper hesitating over a large total is far more likely to complete the purchase when the number they see is a first installment rather than the full amount. By splitting the cost, BNPL reduces the sticker shock that drives cart abandonment, which is why providers consistently report higher checkout completion when BNPL is offered.

It raises the average order value. When affordability is spread over weeks, shoppers trade up: they add the extra item, choose the higher-spec model, or move from a single product to a bundle. Merchants offering BNPL routinely see larger baskets than card-only checkouts, because the perceived cost per payment, not the total, anchors the buying decision.

It widens the addressable customer base. BNPL grows a business's addressable customer base by attracting people who might not otherwise buy. This includes younger buyers who under-index on credit cards, shoppers who want to avoid having to revolve card debt, and people in regions without good access to traditional loans. The BNPL provider takes on the default risk (the chance a buyer won't pay) and pays the store immediately. This allows the store to gain safe incremental sales without worrying about losing money if the customer misses a payment.

The trade-off is the merchant fee. It is usually more expensive for a store to process a BNPL transaction than standard credit card fees (card interchange). Because it costs the store more, BNPL is most effective when it actually convinces hesitant shoppers to buy or encourages them to spend more. The goal isn't just to add it to every single checkout, but to use it strategically to measure incremental lift (the actual, measurable increase in new sales) rather than subsidizing customers who were going to pay in full anyway.

Which industries benefit most from BNPL globally?

BNPL's value concentrates in categories where price is a barrier and the purchase is considered rather than impulsive. Globally, a few verticals stand out.

- Fashion, apparel, and footwear. BNPL's original home, and still its largest category. Higher basket values, try-before-you-commit behaviour, and a young, style-driven customer base make it a natural fit, and installments meaningfully lift both conversion and order size.

- Electronics and consumer tech. High-ticket, considered purchases such as phones, laptops, and appliances are where spreading the cost has the strongest effect on the decision to buy now rather than wait.

- Travel and hospitality. Flights, packages, and hotel stays are large, planned outlays that suit installments well, and BNPL for travel is a fast-growing global segment as providers and orchestration platforms add travel-specific flows.

- Health, wellness, and beauty. Elective and semi-discretionary spend, from dental and optical to cosmetics and fitness, converts strongly when broken into affordable payments, and is a major BNPL use case in the Gulf in particular.

- Home, furniture, and big-ticket retail. Furnishings and home improvement combine high values with planned buying, making installments an effective conversion tool.

- Education and essentials in emerging markets. In markets like Saudi Arabia, BNPL is widely used for essentials such as education and medical costs, extending its role well beyond discretionary retail.

The common thread is that BNPL works best where the total price would otherwise stall the sale. For low-value, impulse, or thin-margin categories, the merchant fee rarely justifies it.

Where does BNPL regulation stand region by region?

Across the markets where most cross-border commerce happens, regulators are moving in different directions and on different timelines, from full licensing regimes already live to deliberate non-regulation. The table summarises the state; the sections that follow give merchants only what they need to act on.

| Region | Status | Key date | The merchant takeaway |

| Australia | Live and enforced | 10 June 2025 | Approvals now include affordability checks; expect fewer instant approvals |

| United Kingdom | Rules published, live soon | Regulation Day 15 July 2026 | Only FCA-authorised providers can operate; verify your provider's status |

| European Union | Transposing into law | Applies 20 November 2026 | Rules differ by country; a bloc-wide rollout is 27 national variants |

| United States | Reversed | Rule withdrawn May 2025 | Federal certainty gone; watch for state-by-state rules |

| Middle East (UAE, Saudi Arabia) | Live and licensed | UAE Sept 2023 onward | Use only central-bank-licensed providers; adoption is very high |

| Southeast Asia (SG, MY, ID) | Mixed regimes | MY law Mar 2026; ID Jan 2027 | One provider can face three different regimes across the region |

| India | Framework live | Effective 8 May 2025 | BNPL sits inside RBI digital lending rules; bank/NBFC-anchored |

| Brazil | Deliberately light touch | Rule dropped Dec 2025 | Market-led; instalments are a cultural default, not a regulated product |

Australia: BNPL is now regulated credit

Australia was the first major market to regulate BNPL outright. From 10 June 2025 it is regulated under the National Consumer Credit Protection Act, and providers must hold a credit licence and meet responsible lending obligations. For merchants, the practical change is that approvals now involve affordability checks, so the near-instant, no-questions approvals of the early years are gone. Adoption is deep, so BNPL remains a must-offer method; just expect slightly higher decline rates and plan a fallback.

United Kingdom: only authorised providers, from July 2026

UK regulation begins on 15 July 2026, following the FCA's final rules. From that date, providers must be FCA authorised, run affordability checks, and give customers Ombudsman access. Merchants that simply offer BNPL at checkout are not the regulated party, but their exposure is real: lending without permission after Regulation Day is not allowed, so the one thing to check is that your BNPL provider is authorised or covered under the temporary permissions regime.

European Union: one directive, 27 national versions

The EU is bringing BNPL into consumer credit law through the Second Consumer Credit Directive (CCD2), which applies from 20 November 2026 and pulls third-party BNPL into the regulated perimeter for the first time, with creditworthiness checks and standardised disclosures required. The merchant takeaway is that CCD2 is a directive, not a single rulebook, so late-fee caps and details vary by country. A single BNPL rollout across Europe is really 27 national implementations, and demand is worth the effort: in Germany, BNPL already outstrips cards in online shopping.

United States: from a federal rule to a state patchwork

The US moved toward regulation and then reversed. The CFPB withdrew its 2024 rule that treated pay-in-four BNPL like credit cards and confirmed it would not reissue it. For merchants, this means less federal certainty and a likely patchwork of state-level rules to watch, in a market where BNPL is already mainstream and a standard checkout expectation.

Middle East: licensed early, adoption very high

The Gulf regulated BNPL ahead of most of the world by treating it as short-term credit. The UAE brought BNPL under central-bank licensing from September 2023, and Saudi Arabia's SAMA licenses providers directly. The merchant takeaways are twofold: use only licensed providers or licensed-bank partners, and lean in, because adoption is among the highest anywhere, with around 77% of Saudi consumers having used BNPL, often for essentials. Sharia-compliant, interest-free structuring is standard, so the product is designed to fit local expectations.

Southeast Asia: three markets, three regimes

Southeast Asia is the most internally varied region on the map. Singapore runs a voluntary industry code with an accreditation mark, Malaysia's Consumer Credit Act 2025 brings BNPL under formal licensing from 2026, and Indonesia is adding age and income eligibility rules from January 2027. For a merchant selling across the region, the single practical point is that one BNPL provider can face a voluntary code in one country, a licensing regime in the next, and hard eligibility limits in a third, so coverage and approval behaviour will differ market by market.

India: BNPL inside the digital lending rulebook

India regulates BNPL not with a dedicated law but by folding it into its broader digital lending regime. The RBI's Digital Lending Directions, effective May 2025, govern how app-based credit including BNPL is originated and serviced, and earlier caps on default-loss guarantees and the ban on loading credit lines onto prepaid instruments reshaped the market. The takeaway for merchants: Indian BNPL is now firmly- bank and NBFC-anchored, so partner through providers aligned with regulated lenders rather than standalone models.

Brazil: a cultural default, lightly governed

Brazil is the deliberate counterexample. Installment buying ("parcelamento") is a long-standing part of Brazilian commerce, and in December 2025 the central bank chose not to impose a uniform framework on installment payments over the Pix rail, keeping the market largely self-directed. For merchants, Brazil's lesson is that "regulatory state" does not always mean more rules: installments are a consumer expectation here, delivered through Pix, cards, and BNPL alike, and the winning move is to offer the local installment methods shoppers already default to.

Why the divergence matters for merchants

For a merchant in one country, BNPL regulation is its provider's problem. For a merchant selling across several, it becomes an operational one, because the same checkout button now behaves under eight different rulebooks at once. Affordability checks are mandatory in some markets and absent in others, so approval rates differ. Licensing decides which providers can even operate, and when. A provider that is fully compliant and converting in one market may be restructuring, withdrawing, or absent in another.

The practical reality is that a merchant's BNPL coverage is only as good as the provider that is live, licensed, and converting in each specific market on each specific day. When a provider tightens checks or exits a market to manage compliance costs, conversion at that checkout drops, and the merchant absorbs the loss unless an alternative is already in place.

How payment orchestration keeps BNPL working across markets

A payment orchestration layer is the structural answer to a fragmented rulebook, because it decouples the merchant's checkout from any single BNPL provider. Rather than integrating one provider per market and re-engineering each time a rule shifts, a merchant connects once and routes each transaction to a provider that is live and compliant in the relevant market.

Juspay, which orchestrates payments across 150+ countries and processes more than 300 million transactions a day, sits in exactly this position, with teams across the regions this map covers: Singapore for Southeast Asia, Dublin for Europe and the UK, Dubai for the Middle East, São Paulo for Latin America, San Francisco for the US, and its Bengaluru headquarters for India. Its orchestration layer connects to 300+ payment providers and local methods, including BNPL, through no-code integrations, so a merchant can add, swap, or route around a BNPL provider without rebuilding checkout each time a market changes. When affordability checks slow approvals with one provider, dynamic routing can present an alternative compliant method instead of a hard decline. When a provider withdraws ahead of a licensing deadline, the merchant's coverage does not collapse with it.

The deeper point is that regulatory divergence is now permanent, not transitional. The merchants who handle it well are not the ones who picked the single right BNPL provider; they are the ones whose checkout is built so that no single provider's status, in any single market, can break the buying experience.

Key Takeaways

- BNPL grows merchant revenue on three levers: higher checkout conversion, larger average order value, and access to shoppers underserved by cards, with the provider carrying the credit risk.

- It pays off most in considered, higher-ticket categories: fashion, electronics, travel, health and beauty, home and furniture, and, in emerging markets, essentials like education and healthcare.

- BNPL is moving globally from unregulated novelty to regulated consumer credit, but on sharply divergent timelines: Australia and the Gulf are live, the UK and EU land in 2026, Southeast Asia is mid-transition, India runs it inside digital lending rules, Brazil stays light-touch, and the US has reversed course.

- For cross-border merchants the real challenge is operational, not legal: the same checkout button now runs under multiple rulebooks, and coverage depends on which provider is live and compliant in each market.

- Payment orchestration absorbs this fragmentation by decoupling checkout from any single BNPL provider and routing to whichever one is compliant and converting in each market.

Frequently Asked Questions

How does BNPL help merchants sell more?

BNPL lifts sales three ways: it improves checkout conversion by replacing a large total with a smaller first instalment, it raises average order value because shoppers anchor on the per-payment cost and trade up, and it reaches customers underserved by credit cards. Because the provider pays the merchant upfront and carries the default risk, the merchant captures these incremental sales without taking on the credit downside, in exchange for a merchant fee.

Which industries benefit most from BNPL?

Categories where price is a barrier and the purchase is considered rather than impulsive: fashion and footwear, electronics and consumer tech, travel and hospitality, health, wellness and beauty, and home and furniture. In emerging markets such as Saudi Arabia, BNPL also extends to essentials like education and medical costs. It rarely pays off for low-value, impulse, or thin-margin purchases.

Is Buy Now, Pay Later regulated?

It depends on the country. As of 2026, Australia and the Gulf states regulate BNPL as consumer credit, the UK begins regulation in July 2026 and the EU in November 2026, Malaysia is rolling out licensing through 2026, Singapore uses a voluntary code, India regulates BNPL within its digital lending framework, the US withdrew its 2024 federal rule, and Brazil has opted for a light touch. There is no single global standard.

What should a merchant check before offering BNPL in a new market?

Whether the provider is licensed or authorised in that market, how affordability checks will affect approval rates, and whether a compliant fallback exists if that provider tightens rules or exits. Because rules and provider availability vary by country, the safest approach is to connect through a layer that can route to whichever provider is live and compliant locally, rather than hard-wiring one provider per market.

Is BNPL still growing despite tighter regulation?

Yes. Regulation is reshaping how BNPL operates, by adding affordability checks, licensing, and disclosure, rather than reversing its growth. The market continues to expand globally and is entering a more mature phase focused on profitability and risk management. For merchants, that means BNPL is becoming a stable, expected checkout option rather than a volatile novelty.

How does payment orchestration help with BNPL across countries?

It lets a merchant connect once to a platform that maintains BNPL and other provider integrations across markets, then routes each transaction to a provider that is live and compliant in the relevant country. This decouples checkout from any single BNPL provider, so a regulatory change, provider exit, or stricter check in one market does not break the buying experience or force a re-integration.