The checkout page is where most purchase intent quietly disappears. And the design of this checkout is no longer just a frontend conversion problem. It earns the customer's decision to click pay. The payment infrastructure behind it determines whether that intent becomes an approved order.

Baymard Institute's 2025 cart abandonment benchmark places the average online shopping cart abandonment rate at 70.22% and estimates that USD 260 billion in orders are recoverable in the US and EU through better checkout usability. Cross-border checkout adds another layer of friction: PYMNTS Intelligence reported in 2025 that 72% of merchants see higher failed-payment rates on cross-border transactions than domestic ones, while 55% of customers give up when multiple payment attempts are required.

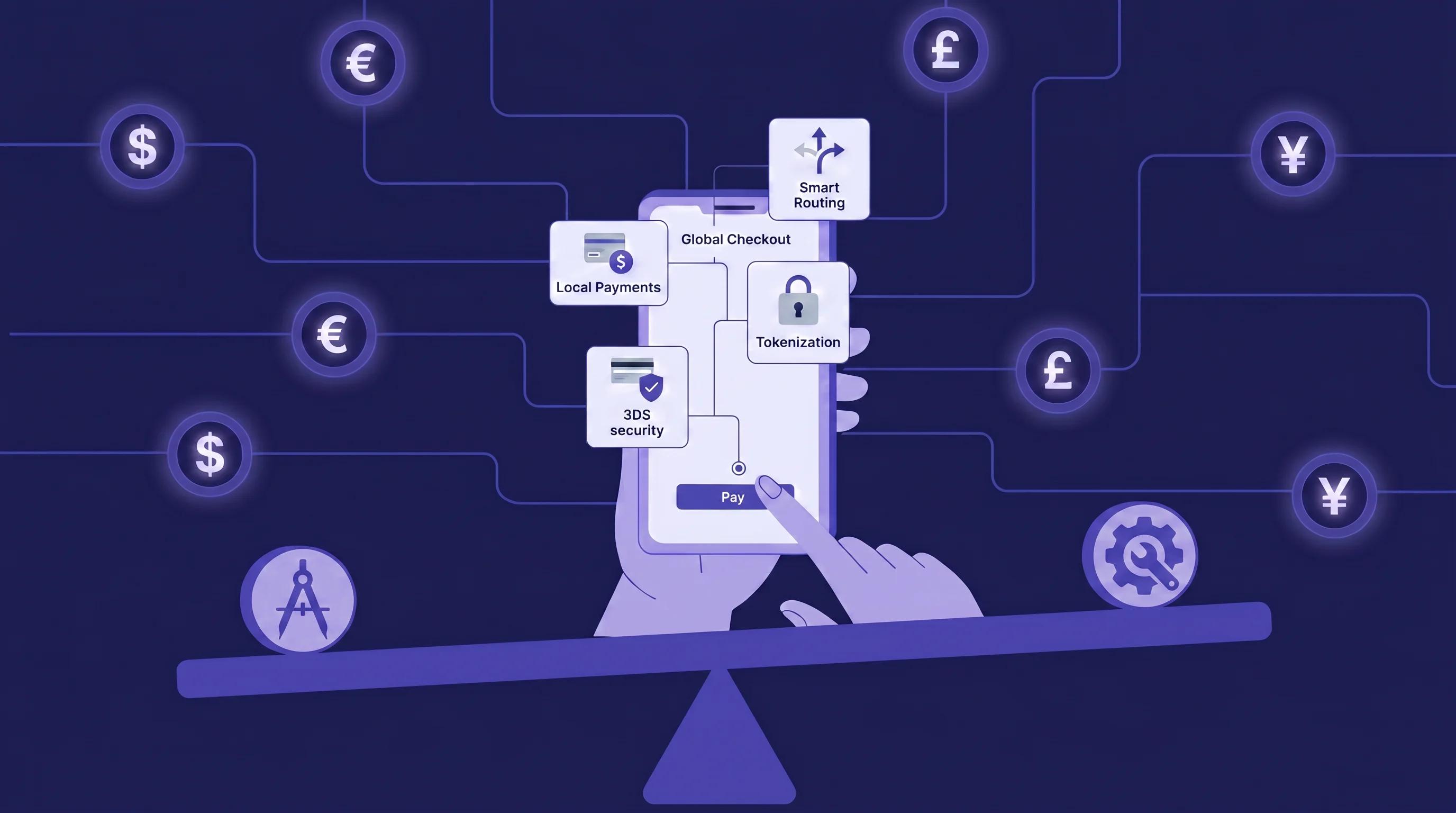

That is why global checkout needs to be designed as one continuous system: user interface, payment method ordering, currency presentation, authentication, routing, tokenization, and recovery. Each layer removes a different reason for failure.

Juspay sees this across large-scale payment flows every day. The platform orchestrates USD 1 trillion in annualized payment volume across 150+ countries, processes 300 Mn+ daily transactions, and runs with 99.999% uptime. That operating vantage point makes one principle clear: checkout design earns the attempt; payment infrastructure earns the approval.

Consider an AI product business selling subscriptions and usage-based plans to customers across the US, Europe, India, Brazil, Japan, and the Middle East. A US buyer may expect cards, wallets, and invoice-friendly flows. An Indian developer may prefer UPI. A Brazilian customer may look for Pix. A European buyer may face Strong Customer Authentication. A Middle Eastern customer may expect Arabic localization, local card rails, or Apple Pay.

For this business, checkout is not just a payment page. It is the revenue-control layer for acquisition, expansion, renewals, and failed-payment recovery.

Why Is Checkout Conversion Both a Design and Infrastructure Problem?

Checkout conversion depends on two linked outcomes: the customer must complete the checkout form, and the submitted payment must be authorized. Frontend design reduces hesitation, typing effort, trust gaps, and the payment-method confusion. Backend infrastructure then handles issuer behavior, network health, authentication rules, routing decisions, and retries.

For the AI product business, a checkout failure can happen before or after payment submission. Before submission, the buyer may hesitate because pricing is not localized, the preferred payment method is missing, or the invoice flow feels unfamiliar. After submission, the payment can still fail because authentication breaks, the issuer declines the card, or the renewal mandate was not captured correctly.

The distinction matters because merchants often optimize only one side. A clean checkout can still lose revenue if payments are routed through a weak acquirer. A sophisticated payment stack can still underperform if customers abandon the page before they click pay.

Baymard's checkout research shows that the average checkout flow in 2024 had 5.1 steps and 11.3 form fields, while most sites need only 8 fields in total. Baymard also found that 17% of users have abandoned it because checkout was too complex. These failures happen before the payment gateway ever sees a transaction.

Once the customer clicks pay, a different class of failure begins. PYMNTS Intelligence reported that cross-border transactions fail more often than domestic transactions for 72% of merchants. At this stage, the cause is more likely local acquiring coverage, issuer risk scoring, unavailable payment methods, authentication friction, or network performance.

The best checkout teams therefore measure both order success rate and transaction success rate. Order success rate asks whether the customer eventually paid. Transaction success rate asks whether each payment attempt succeeded. A card decline followed by a successful wallet payment can produce a 100% order success rate and a 50% transaction success rate. Both numbers tell the truth, but about different parts of the system.

What Are the Five Frontend Principles of High-Converting Checkout?

High-converting checkout design gives customers confidence, reduces unnecessary work, and presents the right payment choice at the right moment. These principles apply across markets before any backend routing or authentication logic begins.

1. Make Checkout Feel Native to the Merchant Brand

A native checkout keeps the customer inside the merchant's visual environment. Fonts, buttons, field labels, colours, error states, and payment method tiles should feel like part of the same product. Sudden redirects to generic gateway pages introduce doubt at the point where trust matters most.

Juspay's checkout experience is built around this principle: merchants can deliver PCI-compliant hosted checkout or API-led flows that match their brand, localize the payment surface, and keep the customer inside a consistent journey.

2. Reduce Fields Before Reducing Steps

Checkout teams often obsess over the number of steps, but Baymard's 2024 research shows that total field count is the stronger usability lever. The average checkout had 11.3 fields, while most sites need only 8.

The practical lesson is simple. Remove fields before redesigning the whole flow. Use address lookup, card type detection, saved payment instruments, inline validation, smart defaults, and clear error recovery. Every field removed lowers typing effort, especially on mobile.

3. Surface the Right Payment Methods First

Payment method ordering should be personalized by geography, device, currency, transaction value, and customer history. A static list creates work for the customer. A relevant list lets them recognize their preferred method immediately.

Stripe's 2025 experiment across 50+ payment methods found that dynamically surfacing at least one relevant payment method beyond cards produced an average 7.4% conversion-rate lift and 12% revenue lift. Stripe also reported that eligible checkouts offering Apple Pay saw an average 22.3% conversion increase.

4. Design for Speed, Especially on Mobile

Checkout speed is a conversion feature. Heavy scripts, delayed payment-method rendering, and redirect-based authentication flows create abandonment risk, especially on mobile networks.

A fast checkout should lazy-load noncritical elements, cache local assets, render preferred payment methods early, and defer risk checks where possible. The goal is not simply a lower page-load metric. The goal is that the customer's preferred payment option appears before intent decays.

On mobile, speed means collapsing input, not just shrinking the layout. Wallets, saved instruments, Click to Pay, local real-time rails, and device-native authentication reduce typing and keep customers inside the merchant context. External redirects break visual continuity, introduce session timeout risk, and make failure recovery harder — native in-app flows eliminate all three problems at once.

Juspay's mobile SDK is deployed on more than 250 million devices, providing deep analytical insights into frontend performance. Minimizing script sizes and caching local assets keeps the checkout loading process well under the critical threshold.

5. Show Failure Risk Before the Customer Clicks

Payment reliability should be visible on the checkout surface. If a bank, wallet, processor, or local payment rail is facing downtime, the UI should guide customers toward a healthier option before they submit a doomed payment attempt.

This is the first bridge from design into infrastructure. The frontend can only show real-time health if the backend is monitoring payment method performance, PSP latency, issuer responses, and regional outages. Once checkout begins to react to payment health, design and orchestration become one system.

How Should Checkout Localization Change From Market to Market?

Checkout localization changes the visible experience and the infrastructure behind it. A market-specific checkout must adapt payment methods, language, currency, authentication rules, refund expectations, recurring-payment rails, and local acquiring paths.

The goal is not to build a separate checkout for every country. The goal is to run one adaptable checkout architecture that can present local choices while routing payments through the infrastructure most likely to approve them.

| Market or Region | What Customers Expect to See | What Infrastructure Must Support |

| United States and Canada | Cards, Apple Pay, Google Pay, PayPal, BNPL, saved cards | Tokenization, wallet support, issuer decline recovery, card account updater |

| European Union | Cards, iDEAL, Bancontact, Klarna, SEPA, Wero in supported markets | SCA strategy, 3DS optimization, PSD2 compliance, PSD3/PSR readiness |

| United Kingdom | Cards, wallets, Pay by Bank, Open Banking flows | Open Banking connectivity, bank availability monitoring, fallback card routing |

| India | UPI, cards, EMI, wallets, UPI AutoPay | In-app UPI flows, recurring e-mandates, bank health monitoring, retry logic |

| Brazil | Pix, cards, installments, wallets, Pix Automatico | Pix QR and copy-paste UX, local acquiring, installment support, recurring Pix readiness |

| GCC and Middle East | Cards, Apple Pay, Mada, KNET, STC Pay, local wallets | Arabic localization, right-to-left layout support, regional network integration |

| Southeast Asia | Cards, PayNow, GrabPay, GCash, QR wallets, bank transfer | Wallet orchestration, QR presentation, local settlement and reconciliation |

| Japan | Cards, wallets, convenience-store payment options, local 3DS expectations | 3DS 2.x readiness, issuer authentication handling, local acquiring |

How Payment Infrastructure Converts Checkout Intent Into Revenue

Once the customer clicks pay, checkout design hands the transaction to payment infrastructure. Five backend principles decide whether that intent becomes revenue: local currency handling, payment orchestration, tokenization with authentication, stored-credential maintenance, and intelligent recovery.

First payments, renewals, and usage top-ups should not be treated as the same payment event. The first payment proves intent and captures consent. A renewal protects recurring revenue. A usage top-up or plan upgrade captures expansion revenue while the customer is already active. Each moment needs a different blend of authentication, tokenization, routing, and recovery logic.

For the AI product business, the click is only the midpoint. The first subscription payment, the next usage top-up, and the renewal charge may each need different infrastructure decisions: currency routing, tokenization, 3DS, card updater checks, mandate handling, retries, or payment links.

These are still checkout design decisions because each one changes what the customer experiences. Currency affects trust before payment. Routing affects whether the attempt succeeds. Tokenization and 3DS affect whether security adds confidence or friction. Stored credentials affect whether renewals fail silently. Retries and payment links decide whether a failed attempt becomes a recovered order.

| Checkout moment | Infrastructure needed | Revenue risk if missing |

| First payment | Currency, payment method, routing, authentication | The customer abandons or the issuer declines |

| Usage top-up or plan upgrade | Stored credential, token, customer consent, risk checks | Expansion revenue gets interrupted |

| Saved-card renewal | Network token, card updater, merchant-initiated charge logic | Subscription churn from outdated credentials |

| Failed attempt | Decline classification, retry path, fallback payment method | A recoverable order becomes lost revenue |

| Cross-border payment | Local acquiring, FX handling, settlement routing | Higher declines, higher cost, harder reconciliation |

1. Treat Currency as the Bridge Between UX and Settlement

Currency is where frontend trust and backend infrastructure meet. Customers need familiar pricing before they pay. Merchants need the infrastructure to manage FX, Dynamic Currency Conversion, settlement currency, provider choice, and reconciliation after the payment succeeds.

PYMNTS Intelligence reported in 2025 that 94% of cross-border shoppers expect to pay in their local currency.

Currency design has three layers. First, show local currency throughout the buying journey, not only at the final payment step. Second, use Dynamic Currency Conversion only when the exchange rate, fees, and customer choice are presented clearly and compliantly. Third, connect the checkout to settlement and routing logic so the merchant can manage FX cost and reconciliation across markets.

2. Route Each Payment Attempt Through the Best Available Path

Payment orchestration improves authorization by routing each payment attempt through the best available path, rather than forcing all traffic through a single PSP or acquirer. For global merchants, orchestration connects checkout intent to payment execution.

A single-PSP setup creates three structural limits. It concentrates outage risk, limits local acquiring coverage, and gives the merchant fewer options when issuers decline transactions. Multi-PSP orchestration gives the merchant more control over routing, fallback, cost, compliance, and recovery.

Smart routing should consider payment method, issuer, country, currency, transaction amount, PSP health, acquirer performance, fraud signals, and past approval patterns. A rule-based fallback is useful during outages, but routing becomes materially stronger when it learns from live performance.

3. Use Tokenization and 3DS to Add Security Without Avoidable Friction

Tokenization and 3DS protect conversion after the customer submits the payment. Tokenization improves security and approval quality by replacing raw card numbers with network tokens. 3DS manages authentication and liability while trying to avoid unnecessary friction.

Visa's 2025 tokenization research reported that tokenized card-not-present transactions had a 4.7% global authorization uplift versus PAN-based card-not-present transactions, along with a 34% average reduction in e-commerce fraud rates. Visa also reported more than 12 billion Visa-issued network tokens deployed by Q1 FY25.

Mastercard announced in June 2024 that it aims for 100% e-commerce tokenization in Europe by 2030 and said its tokenization service secures about 25% of all Mastercard e-commerce transactions globally, with adoption accelerating 50% year over year.

Authentication is moving in the same direction. Europe already requires Strong Customer Authentication under PSD2, and the European Parliament's 2026 legislative train shows PSD3 and the Payment Services Regulation as close to adoption after a provisional Parliament-Council agreement in November 2025.

The merchant objective is not to avoid authentication. The objective is to authenticate intelligently. Low-risk transactions should use exemptions where allowed. Higher-risk transactions should use the least disruptive compliant path. Saved-card and wallet flows should use tokens, passkeys, and device-native signals where supported.

4. Keep Stored Credentials Current for Renewals

Card updater services protect recurring revenue by keeping saved card credentials current when cards expire, are reissued, or are replaced after loss or theft. Visa Account Updater enables credential-on-file merchants to receive updated account information through participating issuers and acquirers, helping reduce the risk of declined transactions from account changes.

For subscription and usage-based AI product businesses, this matters before the retry engine ever runs. Mastercard Automatic Billing Updater supports recurring and credential-on-file payment arrangements when account details change. Combined with network tokens, account updater services turn stored credentials into a renewal reliability layer.

For subscription and usage-based businesses, that first payment often sets up later renewals, plan upgrades, or usage top-ups. The payment stack must recognize when a later charge is customer-initiated versus merchant-initiated, so authentication, tokenization, and retry rules are applied correctly.

5. Recover Failed Attempts With Smart Retries, Payment Links, and Mandates

Recovery begins when the first payment attempt fails. A strong checkout does not treat failure as the end of the session. It classifies the failure, selects the right recovery path, and keeps the customer close to the original purchase intent.

The first distinction is soft decline versus hard decline. A soft decline is temporary: issuer timeout, network latency, insufficient funds, or temporary risk review. A hard decline is structural: invalid card, stolen card, closed account, or permanent issuer refusal.

Decline classification should go deeper than a simple failed-payment label. Common categories include issuer declines, authentication failures, PSP or network timeouts, insufficient funds, expired or reissued credentials, and fraud or risk blocks. Each category needs a different response: retry, reroute, authenticate again, update the credential, or ask the customer for another payment method.

Soft declines can often be retried through another acquirer, PSP, route, or payment method. Hard declines should not be retried blindly because repeated failed attempts add cost and can worsen risk signals. The checkout should instead ask the customer to choose another payment method.

Payment links extend recovery beyond the original checkout surface. They are useful for abandoned carts, assisted commerce, high-consideration purchases, and social commerce. In markets where WhatsApp, SMS, or email are part of the buying journey, a localized payment link can recover demand without forcing the customer back through a full website flow.

How Juspay Approaches Multi-Market Checkout

Juspay approaches multi-market checkout as a single operating layer across localized checkout design, payment orchestration, authentication, tokenization, recurring payments, and recovery. The purpose is to help merchants present a local checkout while operating a globally consistent payments stack.

For a global AI product business, Juspay's role is to make the checkout feel local to each buyer while keeping routing, authentication, tokenization, recurring payments, recovery, and analytics unified behind the scenes.

The frontend layer supports branded checkout, localized language and currency, preferred payment-method ordering, native mobile flows, payment links, and real-time failure guidance. This is where the customer decides whether to pay.

Juspay’s infrastructure layer connects to 300+ PSPs and local payment methods. It manages routing, downtime protection, tokenization, authentication, smart retries, recurring payment support, and unified analytics across markets. This is where the payment attempt becomes an approved order.

Juspay's engineering stack is built for high-volume payment reliability, including multi-multi active-active infrastructure, and progressive rollout mechanisms that start with limited traffic before wider deployment. The aim is not just to make checkout look local, but to make payment execution resilient across markets.

That is the operating model global merchants need. Checkout design earns customer intent. Orchestration, currency logic, tokenization, authentication, and recovery convert that intent into revenue.

Key Takeaways

- Checkout conversion has two jobs: earn the click and win the authorization.

Baymard reports a 70.22% average cart abandonment rate and estimates USD 260 billion in recoverable orders in the US and EU through better checkout usability. - Reducing fields matters: Baymard found the average 2024 checkout had 11.3 fields, while most sites need only 8.

- Dynamic payment-method surfacing works. Stripe found a 7.4% average conversion lift and 12% revenue lift when relevant methods beyond cards were surfaced.

- Currency is the bridge between UX and infrastructure. PYMNTS reports that 94% of cross-border shoppers expect to pay in local currency.

- Tokenization is now an authorization lever, not just a security control. Visa reports a 4.7% authorization uplift for tokenized CNP transactions versus PAN-based CNP transactions.

- Juspay's role is to unify localized checkout design with global payment orchestration across PSPs, payment methods, authentication rules, currencies, and recovery paths.

Frequently Asked Questions

What is global checkout design?

Global checkout design is the practice of adapting checkout UX, payment methods, currency, language, authentication, and payment routing to each market while running one consistent payments architecture. It combines frontend design with backend payment orchestration.

What is the average online shopping cart abandonment rate in 2025?

Baymard Institute's 2025 benchmark places the average documented online shopping cart abandonment rate at 70.22%. Baymard also estimates that USD 260 billion in orders are recoverable in the US and EU through better checkout usability.

Why do payment methods affect checkout conversion?

Payment methods affect conversion because customers are more likely to complete checkout when they see familiar, trusted ways to pay. Stripe's 2025 experiment found that surfacing at least one relevant payment method beyond cards lifted conversion by 7.4% on average.

Why is currency conversion important in cross-border checkout?

Currency conversion is important because shoppers need price clarity before they pay, while merchants need backend controls for FX, settlement, routing, and reconciliation. PYMNTS reported that 94% of cross-border shoppers expect to pay in local currency.

How does smart routing improve payment success?

Smart routing improves payment success by sending each transaction through the PSP, acquirer, or payment path most likely to approve it. It can respond to issuer behavior, PSP downtime, local acquiring needs, and payment method performance.

Does network tokenization improve authorization rates?

Yes. Visa's 2025 research reported a 4.7% global authorization uplift for tokenized card-not-present transactions compared with PAN-based card-not-present transactions. Visa also reported a 34% average reduction in e-commerce fraud rates for tokenized transactions.

What is a card updater service and why does it matter for subscriptions?

A card updater service keeps stored card credentials current when a card expires, is reissued, or is replaced. Visa Account Updater and Mastercard Automatic Billing Updater help credential-on-file businesses reduce renewal declines caused by outdated card details.

How does Juspay differ from a single-PSP checkout setup?

Juspay combines localized checkout design with payment orchestration across 300+ PSPs and local payment methods in 150+ countries. A single-PSP setup can process payments, but orchestration gives merchants more control over routing, failover, authentication, tokenization, card updater services, and recovery.