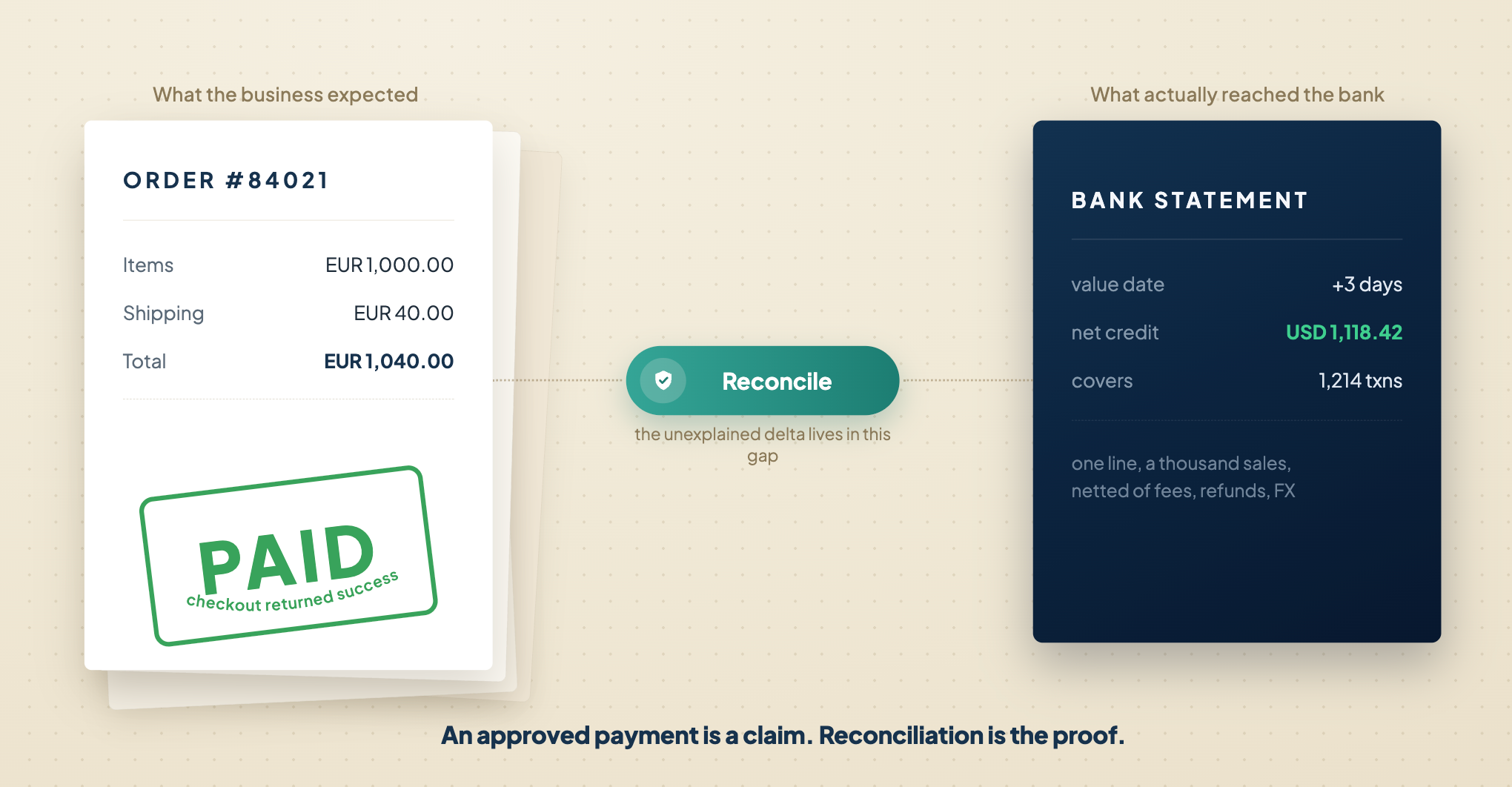

An approved payment can still become a finance exception.

A merchant records an order as paid the instant the checkout returns success. The payment service provider may capture that payment hours later, place it in a settlement batch on a different day, deduct several fees, and send a single net bank credit covering thousands of transactions at once. A refund or dispute can then reshape the economics in a later accounting period. The "paid" status the customer saw was true, and the books can still be wrong.

That gap is why payment reconciliation is not a single comparison. It is a chain of controls connecting what the business expected, what each provider processed, what each settlement report declared, and what actually reached the bank.

What is payment reconciliation across multiple PSPs?

Payment reconciliation across multiple PSPs is the process of linking merchant orders to normalized payment events, provider settlement records, fees, refunds, disputes, and bank credits. Its purpose is to prove that every financial event is complete, correctly valued, traceable, and posted to the right account.

At its core, payment reconciliation is the process of matching PSP payouts with internal records such as orders, invoices, or financial statements. That is a useful starting point. At enterprise scale, the control has to answer far more than "does the payout total match?"

It must answer:

- The Reality Check: Did the customer's money actually go through, or was the card just authorized?

- The Math: Was the order charged the right amount and in the correct currency?

- The Route: Which specific payment provider handled this transaction? And which settlement batch contains it?

- The Deductions: Why is the money deposited into the bank less than the sale price? (Tracking the exact fees, explaining the difference between gross and net).

- The Destination: Did the cash actually land in the correct corporate bank account?

- The Aftermath: If a customer demanded a refund or disputed a charge three weeks later, was that money properly subtracted from the original sale record?

These questions get harder the moment a merchant adds providers, local payment methods, currencies, legal entities, and business systems. Picture a travel marketplace operating across Southeast Asia and Europe: it might route cards through one acquirer, accept a real-time rail like UPI or PIX through another, and offer a regional wallet through a third. Each of those sources can use different identifiers, statuses, file formats, cut-off times, and settlement calendars. None of them speaks the others' language.

The payout itself is also an aggregate. In standard PSP architecture, automated settlements consolidate funds across multiple transactions. Which is why a single bank credit usually cannot be matched directly to one merchant order. One line on the bank statement might represent a thousand sales, forty refunds, and a handful of fees, all netted into one number.

Why does an approved payment still fail to reconcile?

An approved payment can fail to reconcile because authorization, capture, settlement, and bank receipt are separate events. They can occur on different dates, carry different references, and be changed by partial captures, refunds, fees, disputes, FX conversion, reserves, or provider corrections.

Looking at standard payment processor event models illustrates the sheer variety of movements that impact a merchant balance, including captures, refunds, chargebacks, FX conversions, rolling reserves, platform fees, and payouts. A reconciliation design that stores only a final payment status loses the evidence needed to explain those changes. When the finance team later asks "why is this batch short by 0.5%?", a single status field has no answer to give.

The lifecycle also runs on more than one clock. An authorization can clear in seconds while the matching bank credit lands three days later, after a weekend.

| Event | What it proves | What it does not prove |

| Authorization | The issuer approved a reservation of funds | That the merchant captured or received the money |

| Capture | The merchant submitted an amount for collection | That it has entered a settlement batch |

| Settlement advice | The PSP assigned financial events to a payout | That the bank has credited the merchant |

| Bank credit | Net cash reached a bank account | That every underlying transaction and deduction is correct |

| Refund | A customer credit was initiated or accepted | That the customer received it or that its settlement deduction is reconciled |

| Dispute | A payment was challenged and may be debited | That the case is resolved or the debit is final |

This distinction matters in every region. Card processors may send batch settlement files on their own cycle. Real-time payment methods can confirm the payment within seconds yet still expose reporting or bank-posting delays. Wallets and alternative methods may run their own settlement cycles and reference structures entirely. A subscription business billing customers in three currencies will see all of these clocks ticking at once.

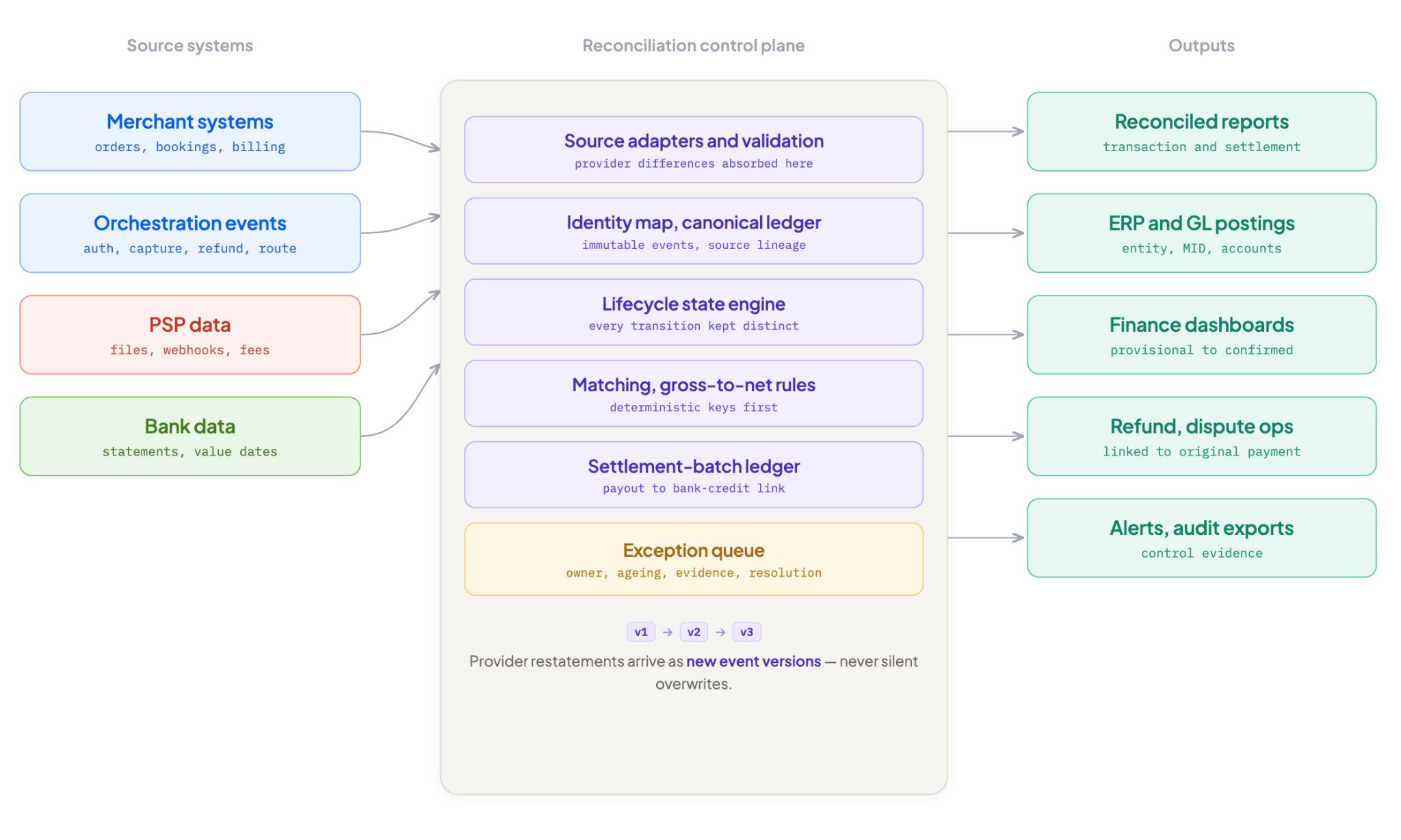

What architecture supports reliable payment reconciliation?

A reliable payment reconciliation architecture uses source-specific adapters, a canonical event ledger, deterministic matching rules, a settlement-batch ledger, bank-credit verification, and an exception workflow. It preserves the original evidence from every source while producing one normalized financial view for operations and accounting.

The principle underneath the architecture is simple: translate every payment provider's data into one standard format immediately, so your accounting team doesn't have to deal with messy, inconsistent data later on.

Which source systems must feed the reconciliation layer?

The reconciliation layer needs commercial, processor, and cash records. No single source can prove the full payment lifecycle, so the architecture should ingest each source independently and retain its lineage.

The minimum source set is:

- Merchant systems: Orders, bookings, invoices, subscriptions, fulfilment, cancellations, and customer references.

- Payment event stream: Authorization, capture, reversal, refund, retry, and routing events from the orchestration or payment layer.

- PSP data: APIs, webhooks, settlement files, fee reports, invoices, dispute feeds, and payout records.

- Bank data: Statement files, transaction feeds, value dates, currencies, and bank references.

- Accounting master data: Legal entity, merchant account, chart of accounts, cost centre, tax treatment, and posting rules.

Every payment provider sends transaction data in its own unique format and on its own timeline. Your system should translate all of this incoming data into one standardized format immediately. Whether one provider sends a daily spreadsheet or another sends real-time code alerts, your accounting software should receive identical, uniform records every time.

What information should your central payment ledger (canonical payment event model) contain?

Your central database should record a permanent history of every financial event, rather than just overwriting the latest status. Each entry should capture the full story: internal order IDs, payment processor references, exact amounts and currencies, timestamps, where the data originated, and how it connects to the final bank payout.

A practical record includes:

- Merchant order, invoice, or booking ID

- Merchant payment and attempt ID

- PSP transaction, capture, refund, or dispute reference

- Event type, status, and version

- Gross amount and currency

- Captured, refunded, disputed, and adjusted amounts

- Fee type, amount, currency, and source

- Processing currency and settlement currency

- Event time, value date, settlement date, and ingestion time

- PSP, acquirer, payment method, MID, sub-MID, and legal entity

- Settlement batch, payout, and bank reference

- Original source file or API object, including its version

An event model also protects history. If a provider restates a batch a week after issuing it, the new record should not silently overwrite the prior evidence. It should create a versioned correction that can be replayed and audited, so a reviewer can see both what was originally reported and what changed.

How should reconciliation matching work?

Matching should use deterministic identifiers first, controlled composite rules second, and manual review for ambiguity. A reconciliation engine should record which rule produced each match and should never hide uncertainty by forcing several plausible records into one result.

A useful hierarchy is:

- Match the merchant payment ID to the PSP reference when both are present.

- Link captures, refunds, and disputes through provider object relationships.

- Match settlement lines to a payout or batch ID.

- Match the payout to the bank credit using provider references.

- Use approved composite keys only when direct identifiers are unavailable, such as amount, currency, merchant account, and a bounded time window.

- Send ambiguous or incomplete cases to an exception queue.

Tolerance rules need restraint. A time window can accommodate delayed posting across a weekend. A rounding tolerance can account for documented FX behaviour. Neither should be used to conceal missing identifiers or unexplained deductions. A tolerance rule that quietly swallows a 2% gap is not reconciliation; it is rounding the truth away.

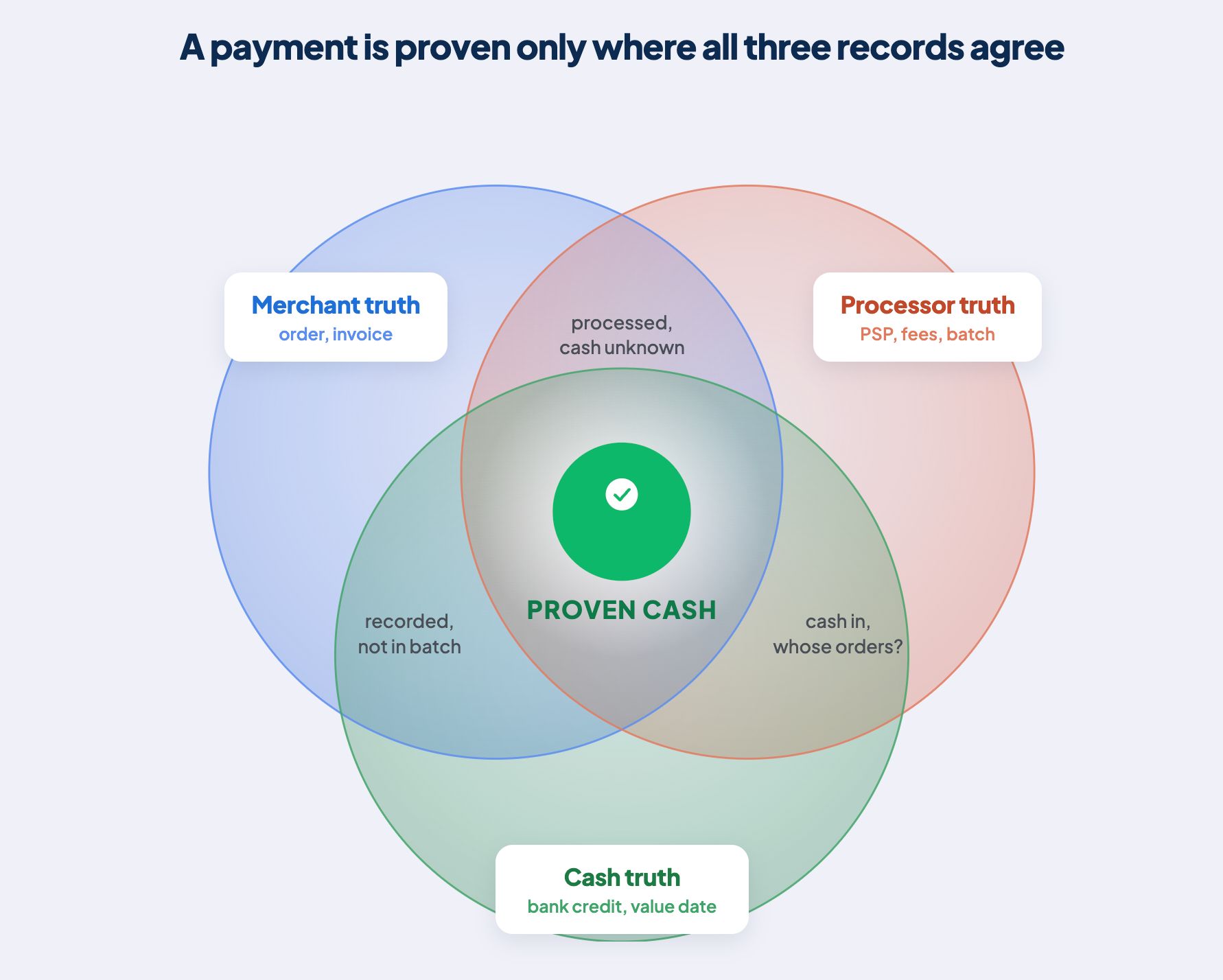

What is three-way payment reconciliation?

Three-way payment reconciliation compares the merchant's order or payment ledger, the PSP's transaction and settlement records, and the bank's record of cash received. A payment is fully reconciled only when the business event, processor accounting, and net bank credit can be connected and explained.

Modern Treasury describes multi-step reconciliation as matching three or more systems of record. In merchant payments, the most useful three-way control is:

| Financial Pillar | Where the Data Lives | Key Question to Answer | How We Track It (Matching Keys) | Where Things Go Wrong (Typical Breaks) |

| 1. Merchant Truth (What we sold) | Internal order, invoice, booking, or subscription database | Did our business correctly record the customer's payment obligation? | Order ID, Invoice ID, Payment ID | The order is marked "Paid" internally, but no payment was actually captured. |

| 2. Processor Truth (What was processed) | Payment gateway (PSP) transaction, fee, and settlement reports | What did the processor actually charge, deduct in fees, and bundle for payout? | PSP Reference ID, Capture ID, Batch ID | A payment was successfully captured, but it is missing from the settlement batch. |

| 3. Cash Truth (What arrived) | Bank statements and direct transaction feeds | Did the expected net cash actually hit our bank account? | Payout ID, Bank Reference Number, Value Date | The processor marks a batch as "Paid," but no deposit ever hits the bank. |

Two-way matching can still be useful. Order-to-PSP matching finds missing or duplicated processing events. PSP-to-bank matching validates cash. The weakness is that either control alone leaves a blind spot. An order-to-PSP check confirms the provider processed the sale but says nothing about whether the cash arrived; a PSP-to-bank check confirms cash but cannot tell you which orders it belonged to. Only the three legs together close the loop.

How should each payment lifecycle event be reconciled?

Every lifecycle transition should be reconciled as its own financial event and linked to the original payment. Updating one mutable "payment status" field cannot explain partial capture, delayed settlement, multiple refunds, dispute debits, or later reversals.

For a merchant to track money accurately across multiple gateways, merchants have to stop viewing a payment as a static event that is simply "successful" or "failed." In reality, money moves asynchronously through a multi-stage lifecycle across your platform, the processor, and the bank. To build a reliable reconciliation engine, your system needs to track every distinct state change along that journey and know exactly what evidence to look for when something goes wrong:

| Lifecycle Event | Merchant expectation (What’s Expected to Happen) | PSP Evidence (Data We Must Capture) | Settlement Effect (Impact on Cash Flow) | Common Exceptions (Where Things Go Wrong) |

| 1. Authorization | The customer's card is approved and funds are placed on hold. | Authorization ID, Status, Expiry Date | None yet (no actual money has moved). | Payment is approved, but the checkout fails and the order is never captured. |

| 2. Capture | We finalize the sale and tell the processor to collect the held funds. | Capture ID, Amount, Currency | Funds get queued up for the next payout batch. | The capture record is partial, duplicated, or missing entirely. |

| 3. Void / Reversal | We cancel the order before funds are collected and release the hold. | Reversal Reference Number, Timestamp | Prevents the customer from ever being charged. | Reversal confirmation arrives after we already cancelled the order internally. |

| 4. Settlement | The processor bundles our captured sales into a scheduled payout. | Batch ID, Itemized Settlement Lines | We are owed the Net Payout (total sales minus fees) | Transactions are missing, assigned to the wrong batch, or tied to the wrong Merchant ID (MID). |

| 5. Bank Credit | The net cash actually hits our corporate bank account. | Bank Reference Number, Currency, Value Date | Money officially lands in our bank (cash leg complete). | Deposit is short, late, bundled unpredictably, or missing completely. |

| 6. Refund | We return money to a customer for a cancelled or returned order. | Refund ID, Status, Amount | Processor deducts the refund from a future payout batch. | Processor marks the refund as accepted, but the financial deduction never happens. |

| 7. Dispute (Chargeback) | A customer tells their bank the charge was fraudulent or wrong. | Dispute ID, Reason Code, Stage, Outcome | Processor instantly debits our account + adds a penalty fee. | The mysterious bank debit cannot be linked back to the original transaction. |

Transaction-level reconciliation can include each payment, refund, chargeback, and its costs, while batch-level reconciliation connects payout batches to bank statements.

Industry reporting standards break down payments into three main stages, including accounting, settlement, and disputes. Your central system needs to track these stages even when different payment providers use their own confusing labels. For example, one provider might call a finished payment "settled" while another calls it "paid out," meaning your system must automatically recognize that both terms represent the exact same financial event.

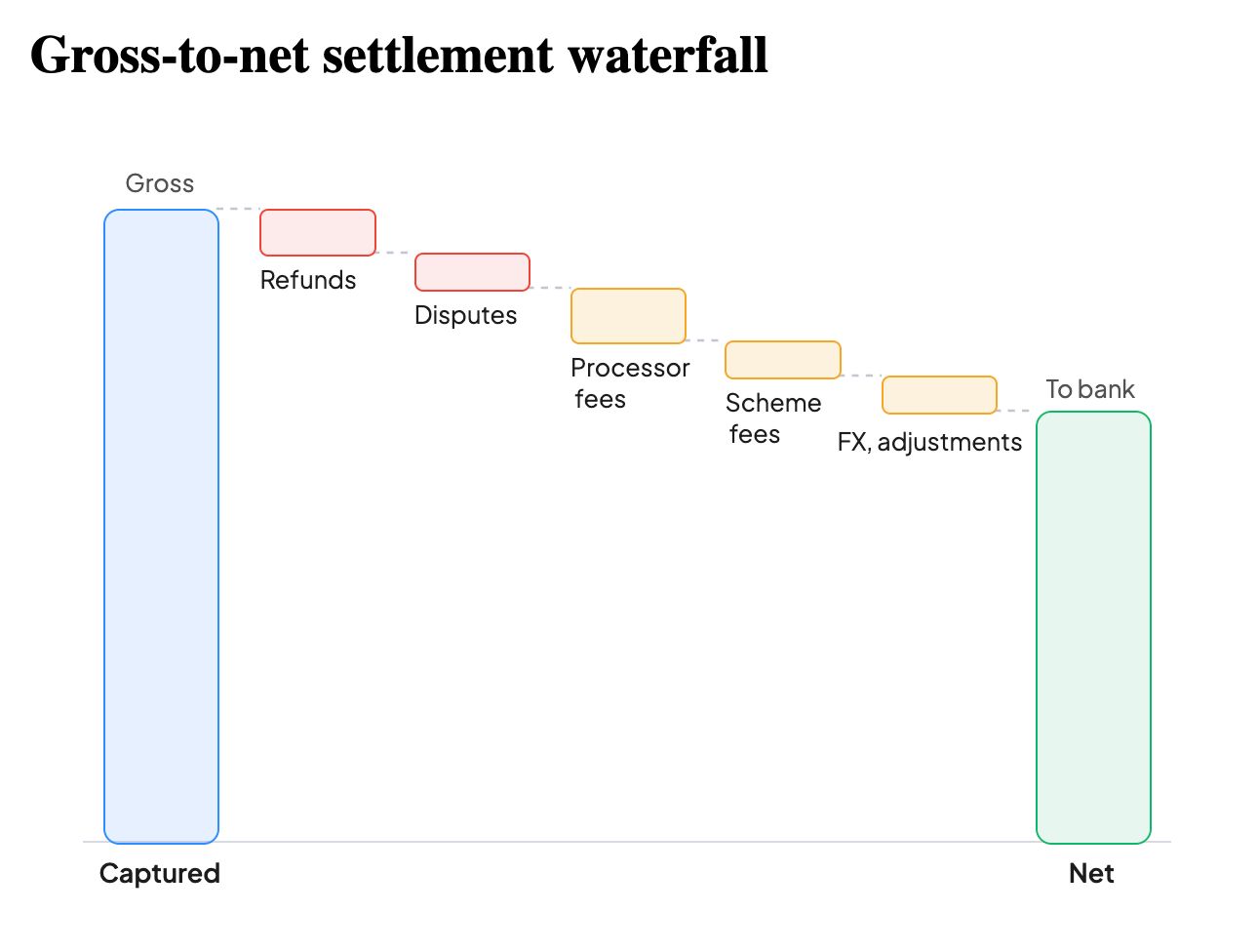

How should fees and FX be reconciled from gross to net?

Fee reconciliation should explain how captured value becomes net settlement at the smallest reliable level available. The model must preserve each deduction's source and currency, because provider reports differ in whether they expose fees per transaction, per batch, or on a separate invoice.

A conceptual calculation is:

The formula is simple. The data rarely is.

One provider may net refunds in the same batch. Another may deduct them later. A dispute fee may arrive before the case outcome. FX may occur between the processing currency and the settlement currency, and the conversion record may use a different date from the original payment. A merchant selling in euros but settling in dollars can see the same sale carry one value at checkout and a slightly different value at settlement, purely from the conversion timing.

Advanced PSP settlement APIs often expose granular provider-level detail including individual payment and payout data, scheme (The underlying card network), interchange, and processor fees. A multi-PSP control plane needs to preserve this depth when it is available, without assuming every provider will supply the exact same fields.

The reconciliation record should distinguish:

- Observed fee: The amount explicitly reported by the provider.

- Expected fee: The amount calculated from a contract or pricing rule.

- Variance: The difference requiring explanation.

- Fee provenance: Settlement file, invoice, API object, or contract calculation.

This supports both accounting and commercial review. It also prevents a recurring and expensive mistake: treating the net bank credit as proof that every underlying fee was correct. The cash can arrive in full while the merchant is quietly being overcharged on interchange.

How are refunds and chargebacks reconciled correctly?

When a customer gets a refund or disputes a charge (Chargeback), don't just delete the original sale from your system. Instead, record the refund as a brand-new transaction tied to the original order. Why? Because the day you approve a refund in your software is rarely the exact day the money actually leaves your bank account.

For a refund, the control should connect:

- The merchant's refund request and approval.

- The PSP refund object and status.

- Any processor or issuer failure returned later.

- The deduction from a PSP balance or settlement batch.

- The customer-facing outcome where that evidence is available.

Partial refunds require one-to-many relationships, because one capture can have several refunds. Think of an electronics retailer refunding a damaged item from a multi-item order, then refunding shipping separately a day later. A failed refund needs its own reversal or returned-funds event rather than a status overwrite, so the history shows the attempt as well as the correction.

Chargebacks have a longer chain: dispute notification, reason code, initial debit, dispute fee, evidence deadline, representment result, and possible credit reversal. Stripe's balance transaction documentation shows why these events must remain distinct: a dispute debit and a later dispute reversal can both affect the balance, and collapsing them into one status erases the money trail.

The reconciliation platform may consolidate dispute data and financial impact, but the acquirer or PSP remains responsible for the underlying dispute process and settlement mechanics.

What causes unmatched payment transactions?

In a multi-PSP setup, unmatched transactions are inevitable. Files get delayed, webhooks fail, and settlement batches cross bank holidays. Most of these breaks come down to missing data, broken ID mapping, lifecycle timing, amount differences, fee or FX treatment, duplicates, or provider restatements. To resolve them quickly, your exception engine needs to do more than flag a generic error. It has to classify the root cause, preserve the evidence, track aging, and route the issue to the right internal owner immediately.

The table below outlines the operational playbook for the 10 most common payment breaks:

| Exception Type | What Actually Went Wrong (Example) | Who Fixes It (Primary Owner) | Immediate First Step (First Control Action) |

| Missing Source | The expected settlement file never arrived from the provider. | Integration / PSP Operations | Check the delivery schedule and API credentials, then re-trigger the file download. |

| Identity Mismatch | Merchant Order ID was never sent to the payment processor. | Payments Engineering | Search using backup identifiers (like customer email or amount), then fix the broken mapping code. |

| Lifecycle Mismatch | A payment was approved (Authorized), but the funds were never collected (Captured). | Payment Operations | Check capture rules and expiration limits to see if the merchant cancelled the order. |

| Amount Mismatch | A partial payment or refund happened at the processor, but wasn't logged in the system. | Finance Operations | Trace the full history of the transaction to reconstruct the missing steps. |

| Fee Mismatch | The payment provider deducted an unexpectedly high fee. | Treasury / Commercial Team | Cross-check the provider's fee report against the agreed contract rates. |

| Timing Mismatch | A payout deposit gets delayed because it crossed a weekend or bank holiday. | Treasury Team | Check the provider and bank holiday settlement calendars to confirm the new arrival date. |

| Currency Mismatch | The currency we charged in (e.g., USD) differs from the currency deposited (e.g., INR). | Treasury Team | Double-check the exchange rate used, the exact conversion timestamp, and any rounding math. |

| Duplicate Data | A single transaction record or system alert was accidentally ingested twice. | Platform Engineering | Automatically filter out the duplicate using the unique source ID and timestamp. |

| Bank Mismatch | A single lump-sum bank deposit combines multiple different settlement batches. | Treasury Team | Break down and match the deposit using payout reference numbers and arrival dates. |

| Restatement | The provider admits a mistake and retroactively changes a past settlement batch. | Finance Control | Log a new versioned correction in the ledger without erasing the original flawed record. |

Payment discrepancies shouldn't vanish the moment someone overwrites a cell. Every resolved break demands a permanent record of the reason, the evidence, the operator, the sign-off, and the final ledger outcome. If you can’t reconstruct the logic behind a fix twelve months later, you haven't built a control. You’ve just built a workaround.

What controls make payment reconciliation audit-ready?

Audit-ready reconciliation is reproducible. A reviewer should be able to start from an order, follow every payment and settlement event, inspect the original source evidence, understand each automated rule or manual decision, and arrive at the accounting entry and bank credit.

The core controls are:

- Immutable source records and file hashes

- Versioned provider corrections and restatements

- Full lineage from source field to canonical field

- The rule and rule version used for every match

- Segregated maker-checker approval for sensitive adjustments

- Role-based access to refunds, overrides, and report exports

- Tracking how long exceptions stay unresolved (exception ageing), alongside clear ownership, comments, and attachments

- Reconciliation reruns that produce the same result from the same inputs

- Retention aligned with legal, tax, audit, and company policy

Real-time visibility is valuable, but it should not be confused with finality. Payment webhooks may update operations immediately while settlement files and bank credits arrive later. The dashboard should label records as provisional, expected, settled, bank-confirmed, or excepted, so nobody mistakes a fast status update for confirmed cash.

How does payment orchestration improve reconciliation?

Payment orchestration improves reconciliation by creating a common identity and event layer across providers. It can centralize PSP data ingestion, normalize lifecycle semantics, preserve routing context, and give finance teams one control surface without taking custody of merchant funds.

Juspay orchestrates payments across 150+ countries and processes 300M+ daily transactions. Its payment orchestration platform connects with 300+ payment providers and payment methods, which gives the reconciliation layer a cross-provider view of transaction context.

That context is what makes investigations fast. A finance team chasing a missing settlement can see not just the final PSP, but also the merchant order, the payment attempt, the routing result, the capture, any refund, and the provider references needed to trace the event end to end. Without that layer, the same investigation means logging into several provider dashboards and stitching the story together by hand.

What should enterprises ask when evaluating reconciliation?

Enterprises should evaluate reconciliation as a financial control system, not a reporting add-on. The assessment should test source coverage, data lineage, three-way matching, lifecycle depth, exception operations, accounting outputs, and the platform's behaviour when evidence is late or corrected.

Ask these questions:

- Which APIs, webhooks, files, emails, invoices, and bank formats can the platform ingest?

- Can it match merchant records, PSP settlement data, and bank credits?

- How are merchant and provider identifiers normalized and preserved?

- How are partial captures, multiple refunds, disputes, and restatements represented?

- Can it preserve transaction-level fees, batch-level fees, FX, reserves, and adjustments?

- How are exceptions classified, assigned, aged, approved, and audited?

- Can outputs follow the merchant's ERP, legal-entity, MID, and chart-of-accounts structure?

- Can every refund or dispute be traced to the original payment and later settlement effect?

- What happens when a file, webhook, or bank credit is late, duplicated, missing, or corrected?

- Does the provider clearly separate reconciliation visibility from responsibility for fund movement?

Building this level of financial observability from scratch requires engineering teams to maintain dozens of fragile gateway integrations, complex lifecycle state machines, and custom exception queues. This is where Juspay comes in. By acting as a single, unified payment control plane, Juspay absorbs provider-specific quirks at the edge and automatically standardizes data across multiple PSPs into one immutable ledger. It delivers the end-to-end three-way reconciliation enterprise finance teams need, which allows you to scale your payment stack without ever losing track of a single rupee.

Key Takeaways

Reliable reconciliation depends on preserving the full financial event chain and proving it against independent records. The strongest design combines a canonical event ledger, three-way matching, explicit gross-to-net calculations, and controlled exception operations.

- Payment reconciliation is a chain of controls connecting business records, PSP events, settlement batches, deductions, and bank credits.

- Three-way reconciliation closes the gaps between merchant truth, processor truth, and cash truth.

- A canonical event ledger should preserve every lifecycle transition and source version.

- Refunds and disputes are new financial events linked to the original payment, not edits to it.

- When a payment breaks, Unmatched transactions require a clear category, an assigned owner, tracked aging, attached proof, and an audited fix.

- Payment orchestration can provide a unified cross-PSP control plane while PSPs and acquirers continue to handle fund movement.

Frequently Asked Questions

What is the difference between payment reconciliation and settlement?

Settlement is the process through which payment funds are calculated and transferred according to the PSP or acquirer's rules. Reconciliation is the control process that verifies the merchant's records, PSP settlement data, deductions, and bank credits agree. A settlement can occur while underlying transactions or fees remain unreconciled.

What is three-way payment reconciliation?

Three-way payment reconciliation compares the merchant's order or payment ledger, the PSP's transaction and settlement records, and the bank statement. It proves that the commercial event was recorded, the processor accounted for it correctly, and the expected net cash reached the merchant's bank account.

How often should a business reconcile PSP settlements?

The appropriate frequency depends on transaction volume, settlement schedules, risk, and close requirements. High-volume merchants commonly need daily controls, with intraday operational monitoring where data is available. Monthly reconciliation alone can allow missing files, short settlements, or incorrect deductions to remain unresolved for too long.

How do you reconcile refunds that settle days later?

Create a separate refund event linked to the original capture, then track its provider status and settlement deduction independently. The refund should remain open until the financial effect appears in a settlement batch or balance record. Failed or returned refunds should create another event rather than overwriting history.

Can payment reconciliation be fully automated?

Most high-confidence matching and report generation can be automated, but ambiguous evidence still requires controlled review. Good automation reduces manual work by routing only genuine exceptions to people. It should not force-match uncertain records, erase source differences, or hide unexplained variances behind broad tolerance rules.

What data is needed to reconcile payments across multiple PSPs?

You need merchant order and payment IDs, PSP transaction references, lifecycle events, gross amounts, currencies, settlement batch IDs, fees, refunds, disputes, payout references, and bank credits. Legal entity, MID, value date, source lineage, and event version are also important for reliable accounting and audit.

How does Juspay support multi-PSP payment reconciliation?

Juspay provides an orchestration and normalization layer across connected payment providers and methods. It can preserve transaction context, consolidate provider data, support matching and exception workflows, and produce unified reporting for finance systems. The connected PSPs, acquirers, and banks remain responsible for processing and moving funds.