Real-time payment systems have reshaped consumer expectations in markets across Asia, Europe, and Latin America. Brazil's PIX is among the most consequential, and it has made Brazil one of the most complex, highest-stakes payment environments on the planet. For global enterprises that process payments across dozens of countries, getting Brazil right is not a regional afterthought. It's proof that your payment infrastructure can operate in the world's most demanding markets.

Brazil has built one of the world's most sophisticated digital payment ecosystems, and one of its most demanding. With PIX commanding 40% of e-commerce payment volume, boleto bancário still active across millions of transactions, parcelamento (installments) embedded in 80% of purchases, and card networks like Mastercard (51%), Visa (31%), and Elo (14%) dividing the remainder, no single payment provider covers everything effectively.

Enterprise merchants entering or scaling in Brazil face a foundational question: how do you manage this complexity without building it yourself?

Payment orchestration, a technology layer that sits above individual gateways and routes each transaction intelligently across multiple providers, is the answer a growing number of global enterprises are turning to. For merchants processing over $100 million annually in Brazil, the difference between a single-gateway setup and a fully orchestrated payment stack can be 10–13 percentage points in authorization rates and millions of dollars in recovered revenue each year.

This post explains how Juspay's payment orchestration platform addresses Brazil's specific payment complexity and what that means in measurable terms for enterprise merchants.

Why Brazil's Payment Landscape Defeats Single-Gateway Setups

Brazil is not a one-method market. It is five or six distinct payment ecosystems running simultaneously, each with its own infrastructure, settlement timing, acquirer relationships, and consumer expectation.

PIX is Brazil's real-time payment system launched by the Central Bank in November 2020. By end-2024, it had 172.6 million users, representing 75% of Brazil's population and processed 57 billion transactions worth USD 3.8 trillion, according to Brazil's Central Bank. PIX now accounts for 40% of all e-commerce payment volume, surpassing credit cards. The June 2025 launch of PIX Automático added recurring debit capability, reducing average merchant transaction costs from 2.34% on credit cards to 0.33% on PIX: a structural shift in how subscription and recurring-revenue businesses operate in Brazil.

Parcelamento (installment credit) is not optional. According to market data, 80% of Brazilian e-commerce transactions are split across 2–12 monthly installments. Consumers expect this at checkout. Merchants that cannot present a clear parcelamento flow, showing per-installment amounts, interest calculations, and total cost, see conversion collapse. A global retailer cannot simply port its European or US checkout into Brazil; parcelamento must be structurally embedded.

Boleto bancário remains relevant, particularly in B2B transactions, higher-value consumer goods, and among consumers without credit cards. Integration requires local banking relationships that most international acquirers don't carry.

Card payments are dominated by Mastercard and Visa, but Elo, a card network operated by Bradesco, Banco do Brasil, and Caixa Econômica Federal accounts for 14% of card volume and requires direct integration to serve Brazil's middle-income segment fully.

International merchants face an additional layer: cross-border settlement, FX conversion costs, and currency display. Merchants pricing in USD and settling through non-Brazilian processors pay a compounding FX spread on every transaction; often 2–4% on top of already elevated processing fees. Orchestration with local acquirer routing and dynamic currency conversion eliminates this spread by settling transactions in BRL through domestic rails.

A single payment provider cannot manage all of this effectively. According to industry data cited in multiple orchestration case studies, Brazil-specific authorization rates for merchants relying on a single international acquirer typically run between 71% and 74%, well below what's achievable with local routing.

What Does Payment Orchestration Actually Do for Authorization Rates in Brazil?

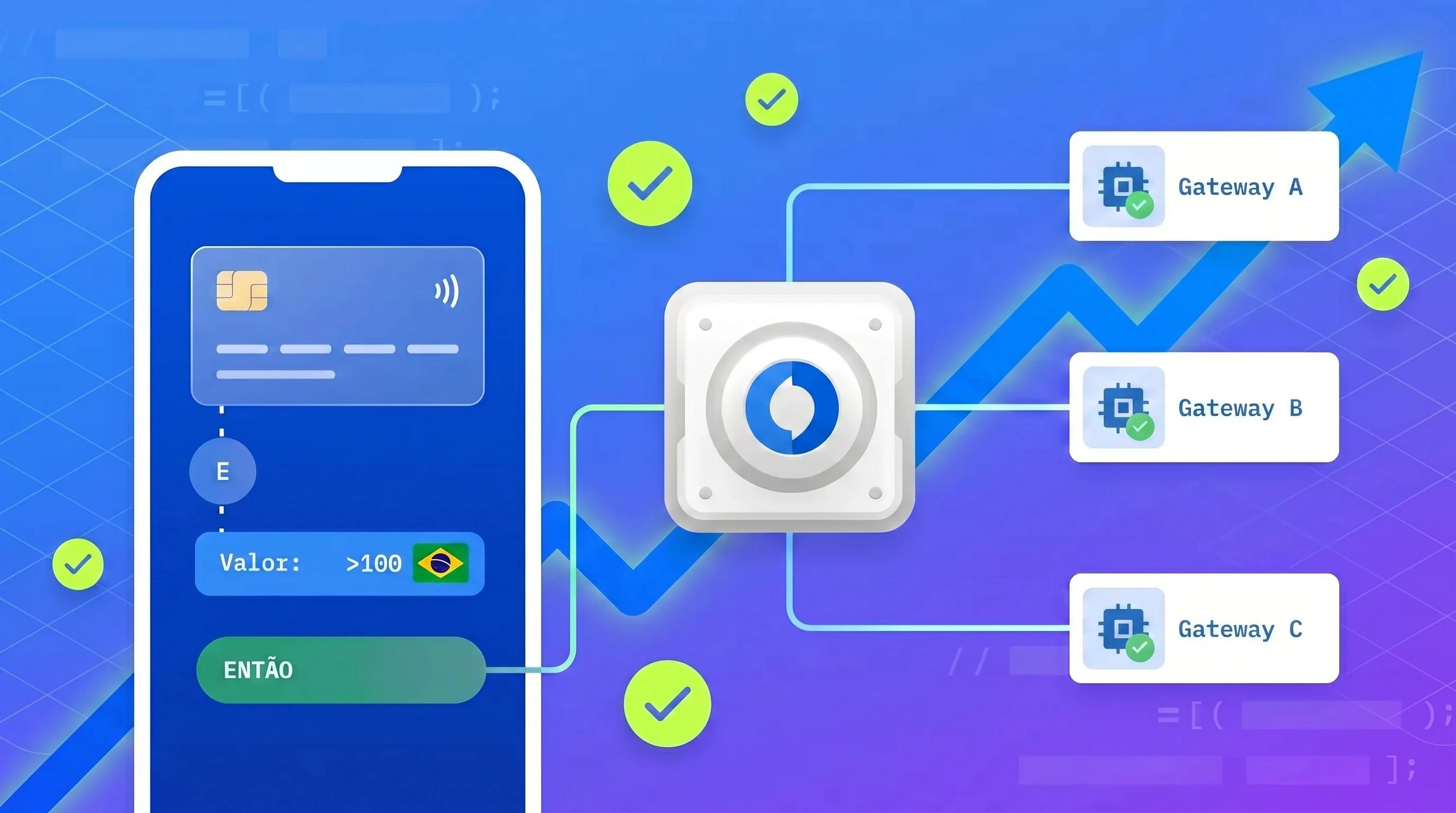

Payment orchestration is a technology layer that connects enterprise merchants to multiple acquirers, PSPs, and payment methods through a single integration, then routes each transaction in real time to the provider most likely to approve it. In Brazil, where authorization rates vary significantly by acquirer, card type, transaction value, and time of day, this routing intelligence has a measurable impact.

Lets look at an example: a marketplace operating across Latin America and Europe implemented an orchestration platform routing Brazilian transactions to local acquirers with PIX and boleto support, and Mexican payments to local banks. Results appeared within 30 days. Brazilian authorization rates rose from 71% to 84%. The marketplace recovered approximately USD 180,000 in monthly revenue from previously failed transactions, according to Payments Strategy Breakdown.

These numbers reflect the structural reality of routing transactions through local rails instead of routing them across international networks that don't have direct relationships with Brazilian issuers.

Juspay, which orchestrates payments across 150+ countries and operates from a dedicated São Paulo office for Latin America, applies the same routing logic at enterprise scale. The platform is trusted by global enterprises including Amazon, Agoda, and HSBC to process millions of daily transactions: the same infrastructure now serves merchants entering Brazil. With 300+ payment providers and methods already integrated and infrastructure processing 300 million daily transactions globally with 99.999% uptime, Juspay's Brazil routing layer selects from multiple local acquirers, PIX rails, boleto providers, and card networks for every transaction in real time.

How Smart Routing Works Across Brazil's Payment Methods

Smart routing in Brazil means different logic for different transaction types. A one-size-fits-all routing rule will underperform because the optimal provider for a PIX transaction is not the optimal provider for a Mastercard parcelamento transaction.

Juspay's orchestration platform applies routing rules along multiple dimensions simultaneously:

By payment method: PIX transactions are routed directly to Brazil's real-time payment rails. Card transactions are split by network (Mastercard, Visa, Elo) and matched to acquirers with the highest approval rates for that card type. Boleto transactions route to providers with local bank relationships for guaranteed settlement.

By transaction value: Higher-value transactions often trigger different issuer risk policies. Orchestration routes these through acquirers with established high-value approval records and applies 3DS authentication where it improves authorization without materially increasing checkout friction.

By acquirer performance: Real-time monitoring detects when an acquirer's approval rate drops (due to a technical incident, batch processing delay, or elevated fraud flags) and reroutes traffic away automatically. This failover capability is critical in Brazil, where acquirer-level incidents can silently depress authorization rates for hours before merchants become aware.

By parcelamento terms: Installment offers are matched to acquirers that have direct relationships with Brazilian issuing banks to confirm the installment plan, ensuring the consumer's chosen payment structure is honored and the authorization succeeds.

This multi-dimensional routing layer is what separates a payment orchestration platform from a simple multi-gateway setup. A gateway switch routes by availability. An orchestration platform routes by intelligence, optimizing for the outcome, not just the connection.

Brazil as a Platform for LATAM Expansion

Brazil's PIX infrastructure is becoming a regional model. Colombia's Bre-B, launched in 2025, was modeled directly on PIX. Bolivia, Paraguay, and Peru are among the regional central banks developing real-time payment rails inspired by the PIX framework. The architectural pattern (instant settlement, open participation, central bank governance) is spreading across the region.

For global enterprises, this means the payment stack built for Brazil has direct applicability across LATAM. Merchants who structure their Brazil payments on an orchestration platform can extend to Colombia, Mexico, and other regional markets without rebuilding from scratch.

Juspay's São Paulo office serves as the company's Latin America hub, with the same global infrastructure (300+ integrated payment providers, 150+ country coverage, and FX optimization across local settlement rails) available as merchants expand from Brazil into the broader region. The institutional knowledge built in Brazil's payment ecosystem transfers directly: real-time payment routing, local acquirer relationships, fraud management tuned for local behavioral patterns, and native-language checkout.

For cross-border merchants, Juspay's orchestration layer also handles FX optimization: routing transactions to local settlement providers that minimize conversion spread, enabling BRL pricing and settlement for international merchants, and eliminating the compounding FX markup that international acquirers typically apply. Merchants entering Brazil from the US or Europe typically reduce their effective cross-border processing cost by 1.5–2.5 percentage points through local routing alone.

For global enterprises, Brazil is not just a market; it's the LATAM proof of concept. Get the payment stack right here, and regional expansion follows the same architecture.

Why Cart Abandonment in Brazil Is a Solvable Problem

Brazil's e-commerce cart abandonment rate reaches 82%, according to the E-commerce Radar: above the global average and driven by payment friction as much as purchase intent. For enterprise merchants, this is the number that translates most directly into lost revenue.

Payment orchestration addresses cart abandonment through three mechanisms:

1. Local payment method coverage. Brazilians who reach checkout and don't see their preferred payment method (PIX, their specific card type, or parcelamento) abandon. According to research cited in multiple payment industry analyses, integrating locally preferred payment methods can boost conversion by up to 30%. Juspay's platform ensures all major Brazilian payment methods are available at checkout, including PIX with a native in-app experience that avoids the redirect friction that drives drop-off.

2. Automatic retry on failure. When a card transaction is declined for a recoverable reason (temporary issuer unavailability, a network timeout, or a soft decline), orchestration retries automatically using a different acquirer before the consumer sees a failure screen.

3. Optimized checkout flow. Juspay delivers custom-branded, native checkout experiences for merchant apps and mobile: localized in Portuguese, displaying prices in BRL with installment breakdowns, and designed for Brazil's mobile-first consumer base. According to PCMI data, 77% of Brazilian online shoppers used mobile shopping apps in the past six months; a checkout experience not optimized for mobile is a conversion problem by definition.

Network Tokenization: Protecting Revenue From Card Churn

Brazil's subscription and recurring-revenue merchants face a specific silent revenue leak: card expiry and replacement. Every time a Brazilian consumer receives a new card (due to expiry, loss, or a bank-initiated replacement) their existing subscriptions linked to the old card number break. The merchant receives a soft decline, the consumer receives no notification, and the subscription lapses.

Network tokenization solves this by replacing raw card numbers with cryptographic tokens issued directly by Visa, Mastercard, and other networks. When a consumer's card is replaced, the network automatically updates the token, and the merchant's stored credential remains valid without any consumer action required.

Juspay's tokenization layer handles this end-to-end through direct relationships with card networks. Merchants using network tokenization typically see 2–3% authorization rate improvements on recurring transactions and a meaningful reduction in churn attributed to payment failure. In a subscription business processing BRL 100 million annually, a 2% authorization improvement is BRL 2 million in recovered revenue.

For Brazilian merchants with high parcelamento volumes, tokenization also improves the authorization consistency of installment plans that span 6–12 months: a card that refreshes its token mid-plan continues processing without disruption.

Fraud Management in Brazil: Local Intelligence, Not Generic Filters

Fraud in Brazil has a specific profile. Foreign merchants applying their existing fraud tools to Brazil typically encounter one of two outcomes: excessive false declines that kill conversion, or excessive approvals that expose the merchant to chargeback liability.

Brazilian fraud requires local behavioral patterns and a CPF (Cadastro de Pessoas Físicas, Brazil's national tax ID) verification layer. International fraud scoring models lack the local transaction history to distinguish a genuine high-value Brazilian consumer from a fraudster using synthetic identity data.

Juspay's orchestration platform integrates with specialized fraud detection providers and applies Brazil-specific risk scoring as part of the transaction routing decision. High-risk signals trigger additional authentication (3DS) while trusted consumer profiles flow through frictionless checkout. This balanced approach (applying friction where it prevents fraud, removing it where it only prevents conversion) is what Juspay's engineering team calls dynamic authentication optimization.

PIX Biometrico (biometric PIX authentication) represents the next layer of this approach in Brazil. Rather than relying on passwords or OTPs for PIX transaction authorization, PIX Biometrico uses fingerprint or facial recognition to authenticate the payer, reducing the account takeover and social engineering fraud that targets standard PIX flows. Juspay's Brazil checkout suite integrates PIX Biometrico where supported by the consumer's device and bank, automatically selecting the appropriate authentication method per transaction.

According to research presented at Authenticate 2025 by Mastercard, payment passkeys (biometric-based authentication) reduce CNP fraud by 2.5x compared to OTPs and authenticate nine times faster, directly addressing the 27% cart abandonment rate caused by slow authentication steps. Juspay's 3DS authentication suite incorporates these capabilities across Brazil's checkout flows.

What Enterprise Merchants Should Expect When Moving to Orchestration

The decision to move from a single-gateway setup to a payment orchestration platform is not a minor operational change for an enterprise merchant. It's an infrastructure replacement. The questions Juspay's São Paulo team hears most from enterprise merchants considering this transition:

How long does integration take? Juspay's platform is designed for enterprise-grade integration with existing payment infrastructure. Most enterprise merchants complete the initial integration in weeks, not months, because the orchestration layer connects to existing systems rather than replacing them. Adding a new payment method (PIX, a local acquirer, a new fraud provider) typically takes days rather than the months required for independent integrations.

How does this affect reconciliation? Orchestration centralizes reporting and reconciliation across all payment providers into a single dashboard. Enterprise merchants managing separate reconciliation flows from three acquirers, a PIX provider, and a boleto processor (each with different settlement timing and data formats) reduce this to one unified view.

What happens if the orchestration platform goes down? Juspay operates a multi-active infrastructure with no single point of failure across data centers and regions: the same architecture that supports enterprises like Amazon processing millions of daily transactions. Every deployment uses automated traffic staggering (rolling out from 1% of traffic upward) with an AB testing framework that benchmarks new releases against stable versions before scaling up or rolling back. The result: a 99.999% uptime track record (less than five minutes of downtime per year), which is the infrastructure benchmark enterprise merchants processing USD 100M+ annually require.

What does this cost? Processing fees through an orchestration platform are typically offset, and often more than offset, by the authorization rate improvements. An enterprise merchant recovering 10 percentage points of authorization rate on BRL 200 million in annual transaction volume is recovering BRL 20 million in revenue that previously failed. Add cross-border FX savings for international merchants, and the net economics of orchestration are strongly positive from the first year.

Key Takeaways

- Brazil's PIX processed USD 3.8 trillion in 2024: real-time payments now dominate the country's payment mix, with PIX accounting for 40% of e-commerce volume.

- Single-gateway authorization rates in Brazil typically run 71–74%; orchestration with local acquirer routing lifts this to 84–85%, a recovery of up to 13 percentage points.

- International merchants pay an additional FX conversion cost of 2–4% on every transaction routed through non-Brazilian processors; local orchestration eliminates this spread.

- Cart abandonment in Brazil reaches 82%, substantially driven by payment failure and missing local methods; orchestration with automatic retry and full local method coverage directly reduces this.

- Network tokenization protects recurring revenue in a market where 80% of transactions use installments spanning multiple months.

- PIX Biometrico and dynamic 3DS authentication are the emerging standard for fraud prevention in Brazil; generic international fraud filters produce false declines or approvals.

- Juspay's platform orchestrates payments across 150+ countries with 300+ integrated providers, 99.999% uptime, and a dedicated Latin America presence in São Paulo: the same infrastructure trusted by Amazon, Agoda, and HSBC globally.

- Brazil is the LATAM proof of concept: payment stacks built and optimized here extend to Colombia, Mexico, and the rest of the region without rebuilding from scratch.

Frequently Asked Questions

What is payment orchestration and how does it improve authorization rates in Brazil?

Payment orchestration is a technology layer that connects merchants to multiple payment providers and routes each transaction in real time to the acquirer most likely to approve it. In Brazil, where authorization rates vary significantly by acquirer and payment method, orchestration lifts approval rates by routing local transactions through Brazilian acquirers with direct issuer relationships, typically from 71–74% to 84–85%, based on documented case studies.

Why do international merchants struggle with payment authorization rates in Brazil?

International merchants routing Brazilian transactions through global acquirers without local bank relationships see systematically lower approval rates. Brazilian issuers are more likely to approve transactions routed through domestic acquirers with established trust relationships and local risk scoring. A merchant relying on a single international gateway also cannot support PIX, boleto, Elo, or parcelamento natively, missing 40–80% of preferred payment methods for Brazilian consumers, and absorbs a 2–4% FX conversion spread on every transaction.

How does PIX Automático change the picture for subscription businesses in Brazil?

PIX Automático, launched in June 2025, enables recurring debit authorizations through PIX, extending the instant payment rail from one-time purchases into subscription billing. This reduces average transaction costs from 2.34% (credit card) to 0.33% (PIX) for recurring charges. For subscription businesses, this is a structural cost reduction. Payment orchestration platforms like Juspay can route recurring transactions to PIX Automático and fall back to card billing when needed, maximizing both cost efficiency and payment success.

What is parcelamento and why must enterprise merchants support it in Brazil?

Parcelamento is Brazil's installment credit system, where consumers split purchases across 2–12 monthly payments. According to market data, 80% of Brazilian e-commerce transactions use parcelamento. Supporting it requires structuring checkout to display per-installment amounts, total cost, and interest calculations, and routing the single authorization to an acquirer that can process the installment plan with Brazilian issuing banks. Merchants that don't support parcelamento structurally lose conversion to competitors who do.

How does Juspay's payment orchestration differ from a standard payment gateway for Brazil?

A payment gateway provides a single connection to payment networks. Juspay's orchestration platform sits above multiple gateways and acquirers, routing each transaction in real time based on approval probability, cost, fraud risk, and payment method. For Brazil specifically: PIX routing through the Central Bank's real-time rails, card routing to the local acquirer with the highest approval rate for that card type and transaction value, boleto routing to providers with local bank settlement relationships, and PIX Biometrico for fraud-sensitive flows, all simultaneously, through a single integration.

What fraud challenges are specific to Brazil, and how does orchestration help?

CNP fraud and PIX disputes drive most of this. International fraud scoring models lack the local behavioral data to distinguish genuine Brazilian consumers from synthetic identity fraud. Juspay's orchestration layer integrates Brazil-specific fraud detection, applies CPF verification, uses dynamic authentication (adding 3DS friction for high-risk signals), and supports PIX Biometrico for biometric-authenticated PIX flows, reducing false declines while preventing actual fraud.

How quickly can an enterprise merchant integrate Juspay's platform for Brazil?

Most enterprise merchants complete initial integration in weeks. Adding Brazil-specific payment methods (PIX, local acquirers, boleto) typically takes days through Juspay's pre-built integrations, compared to months for independent development. Juspay's São Paulo team works directly with Brazilian merchants through the integration and ongoing optimization process.

Is Juspay's payment orchestration platform PCI DSS compliant for Brazil?

Yes. Juspay's platform is built with PCI DSS compliance as a core requirement. Network tokenization replaces raw card data with secure network tokens, keeping merchants out of PCI DSS scope for stored card credentials. Juspay's multi-active data center infrastructure ensures compliance obligations are met continuously, and addresses LGPD (Brazil's Lei Geral de Proteção de Dados) data residency requirements through local processing and storage architecture.